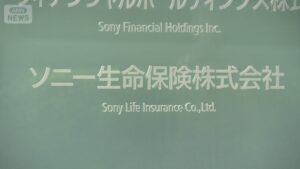

TOKYO (TR) – Earlier this month, Prudential Life Insurance Co., Ltd. revealed that current and past employees inappropriately received over 3.1 billion yen from nearly 500 customers.

At the press conference on January 23, president Kan Mabara apologized: “We sincerely and deeply apologize for the great anxiety and inconvenience caused to our customers and others who were victimized by the discovery of serious inappropriate conduct over many years.”

Mabara also announced that a third-party committee would be established to provide compensation to customers. As well, he has resigned from his post, effective on February 1.

Obviously, the story does not end there. Since the revelations became public, various tabloids have issued reports as to what actually went on at Prudential Life. In summary, it was a large-scale fraud carried out by aggressive salespeople that manipulated a system lacking oversight.

Repeated arrests

Founded in 1987, Prudential Life utilizes a uniquely aggressive sales style for its sales representatives, who are known as “Life Planners.” As a result, the company has generated approximately 3.8 trillion yen in premium and other income, rivaling Sumitomo Life Insurance to make it one of Japan’s leading life insurance companies.

Shortly after its start, that aggressive sales approach got out of control. Those past and current employees involved in the fraud made fictitious investment offers to policyholders and potential customers, promising principal guarantees and high returns, and then had them transfer money into their accounts. Some victims suffered losses in the tens of millions of yen, and lawsuits have been filed against the company.

Prudential Life began its internal investigation in August 2024, triggered by the repeated arrests of former employees on suspicion of fraud, reports weekly tabloid Shukan Bunshun (Jan. 29).

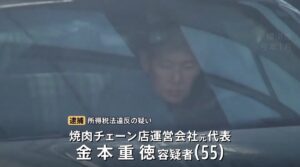

“In June 2024, Ishikawa Prefectural Police arrested a former employee in his 60s for defrauding Prudential Life customers under the guise of investment management,” a social affairs reporter explains.

There were 34 victims with losses totaling 750 million yen. In September of the same year, another former employee in his 30s was arrested on suspicion of fraud for making fictitious investment offers.

The Financial Services Agency became concerned by the string of these fraud cases. In April 2025, it ordered Prudential Life and its Japanese holding company to issue a report under the Insurance Business Act.

Furthermore, it was discovered that Prudential Life had received inappropriate payments through methods unrelated to its insurance operations.

“Since 1991, a total of 106 current and former employees approached a total of approximately 500 customers with investment and profit-making opportunities in cryptocurrencies and other assets, and embezzled the money they received. Numerous cases were also found in which the employees borrowed money and never paid it back,” the reporter says.

These employees received a total of approximately 3.08 billion yen. Of that, approximately 2.29 billion yen has not been returned to customers.

In one case, a woman sued a female employee who had sexual relations with her husband in securing a deal, a practice referred to ask makura eigyo (pillow sales).

Another female victim tells her story in a later report on the online site of Bunshun (Jan. 24). After meeting a Life Planner at an izakaya restaurant, she signed up for insurance.

“[The LP] was always living a life of luxury, even paying for other customers’ bills at restaurants,” she says. “I also remember him bragging about ‘paying his mistress’s rent’ despite being married.”

However, six months later, he asked her for money for divorce mediation. She wound up lending him 1.23 million yen, which he promised to pay back.

“I trusted him because of the company’s title, Prudential Life, and his lavish lifestyle,” she says.

The money was never returned.

Severance package of nearly 100 million yen

In response to the misappropriations, Mabara tendered his resignation. He announced that he would be replaced by Hiromitsu Tokumaru, President and CEO of group company Prudential Gibraltar Financial Life Insurance. However, Mabara will remain with the company in an “advisor” role.

A former employee of the company is outraged at the reshuffle.

“Despite the fact that such a major issue has come to light, president Mabara will be paid a severance package of nearly 100 million yen,” the former employee says. “He is also expected to receive stock options worth around 150 million yen. And yet, it’s inconceivable that he intends to stay on at the company as an ‘advisor.'”

When Bunshun asked Prudential Life for comment, the company gave the following response: “[Regarding the president’s appointment as an advisor], given that the transition has not been fully completed, we will support the management team in implementing measures to prevent a recurrence until the end of July. Mabara plans to resign from his advisory position at the end of July.”

In addition, the aforementioned press conference did exactly inspire confidence that some sort of rehabilitation will take place at Prudential Life.

An economics reporter says: “The day of the press conference saw the dissolution of the House of Representatives and a press conference by the Bank of Japan Governor. Prudential Life likely arranged the schedule to minimize the coverage of their press conference. Furthermore, the ability to ask questions at the conference was limited to Bank of Japan Press Club member companies and business magazines with which they regularly have contact. At the last minute, freelance and magazine reporters were finally allowed to ask questions, but their handling of the situation seemed extremely dishonest.”

Plagued by scandals

Japan’s life insurance industry has been plagued by scandals in recent years.

Six years ago, a case of fraud of approximately 1.9 billion yen by a former special investigator at Dai-ichi Life Insurance was uncovered. The woman had proposed fictitious financial transactions to a total of 24 customers.

In 2011, a former sales representative at Nippon Life Insurance was discovered to have proposed a fictitious insurance contract to a woman in her 90s and defrauded her of approximately 15.32 million yen.

The next year, it was discovered that a former sales representative at Meiji Yasuda Life Insurance had defrauded 10 customers of approximately 130 million yen.

In March 2013, Taiki Life Insurance announced that a former sales representative had defrauded customers of approximately 81.3 million yen. Nine months later, Meiji Yasuda Life Insurance announced that a former sales representative had defrauded approximately 200 million yen.

“Excessive respect for salespeople”

As alluded to previously, Prudential Life’s sales model is unique in the life insurance industry, with Life Planners managing sales accounts, reports the online site for Spa! (Jan. 25).

After a certain period of time, Life Planners are placed on a full commission system, or performance-based compensation. If they secure many contracts and achieve high performance, they can earn annual compensation in the hundreds of millions. However, if their performance is poor, their salary will be lower.

The results of its internal investigation as revealed on January 16 mentioned this compensation system.

“A compensation system that was excessively linked to performance attracted personnel with a financially focused mindset, and the instability of salespeople’s income increased the risk of inappropriate behavior,” the report found.

It went on, “An organizational culture of excessive respect for salespeople, an absolute emphasis on the business model, and high praise for high performers had been cultivated.”

It added, “In sales systems, salespeople are primarily evaluated based on the number of new contracts they secure and maintain. Therefore, salespeople with good performance, higher qualifications, and numerous awards are likely to be perceived as having earned the respect and trust of customers, and as a result, they tend to have a greater say.”

A former Prudential Life employee says, “When I was there, there were no restrictions other than being required to come to the office once or twice a week, and each sales representative was free to act as they pleased. The basic pattern was to make sales through referrals from acquaintances and policyholders, and unlike major domestic insurance companies, many of our policyholders were relatively high-income earners, such as business managers, private practice physicians, lawyers, employees of foreign companies, and people in other specific professions. For example, business managers are often connected to many fellow business managers, and through referrals they can gain strong connections and expertise in that world, making it easier to secure contracts.”

The average annual salary for an employee is usually 10 to 20 million yen. “But you have to keep signing new contracts at a rate of at least one per week, which is quite tough. Conversely, those who can’t produce that kind of results will quit, so employees who are capable enough to survive will earn that much,” the same former employee says.

There is no real quota system.

“If performance doesn’t improve,” the former employee says, “salaries simply decrease, but the company rarely presses employees. If the salary becomes so low that it’s unlivable, employees can simply quit and find another job, so I personally feel that in some ways it’s a fair environment. While I mentioned freedom in work style earlier, as a financial institution, financial transactions with customers and third parties involved in insurance solicitation are strict, and borrowing or receiving money from customers is prohibited by company rules. If discovered, employees have no right to complain even if they are fired. The training system is comprehensive, making it a good environment for those who want to improve their financial knowledge. Also, when I was there, there was a system in place that invited top performers and their families to an awards event at a luxury hotel in Hawaii once a year, and there was also an incentive of a trip to Hawaii on company funds.”

“Undermine the company’s competitiveness”

In the aforementioned report, Prudential Life listed measures to prevent recurrence such as “fundamental improvements to incentive structures such as sales compensation systems” and “strengthening systems to properly understand and manage when, where, to whom, and what sales activities sales employees are conducting.”

The aforementioned employee is skeptical.

“Prudential Life’s competitive edge lies in its high compensation, which is based entirely on commission,” the former employee says. “Any major changes to this compensation system would significantly lower employee motivation, and its best salespeople would likely move to other companies or industries where they could receive higher compensation.”

Furthermore, the company’s salespeople close deals by building relationships with customers.

“This is done in various ways. Even on weekends and late at night, they go golfing or out drinking with them,” the aforementioned employee says. “Therefore, controlling or restricting these behind-the-scenes sales activities, such as restricting excessive socializing in private, would significantly undermine the company’s competitiveness.”